Most "agentic AI startup" lists read like a press release compilation: company name, one-line description, funding amount, next. Magical's widely shared "14 Top Agentic AI Startups" is a perfect example. Fourteen companies, surface-level descriptions, no evaluation criteria, no integration analysis, no guidance for the healthcare CTO who actually needs to choose between these vendors.

We are going deeper. This guide covers 20 companies, organized by healthcare use case, with real funding data, integration capabilities (FHIR, HL7, EHR connectivity), measurable outcomes, and a practical evaluation framework. We have built integrations against many of these platforms and evaluated others for clients. This is what we actually think, not what their marketing teams want you to believe.

The healthcare AI market crossed $10.5 billion in funding in 2024 alone, with AI-enabled companies now capturing 54% of all digital health funding. In 2026, the hype-to-reality transition is complete. Capital is flowing toward companies that demonstrate measurable productivity gains and clinical ROI, not just impressive demos. Sixty-one percent of healthcare leaders say they are already building agentic AI initiatives, and 85% plan to increase investment over the next two to three years.

Here are the 20 companies that matter most right now, and exactly how to evaluate them.

The Funding Landscape: Where the Money Is Going

Before we break down individual companies, the funding data tells a clear story about where investors see the highest-conviction opportunities in healthcare AI. Among the 15 agentic AI startups that closed rounds in late 2025 or early 2026, the average round size reached $155 million, nearly double the $82 million average from the first half of 2025.

Clinical documentation leads in total capital deployed, with Abridge alone raising over $800 million. But the fastest growth is in RCM and prior authorization, where companies like Adonis are posting 4x revenue growth, and Cohere Health is processing over 12 million authorization requests annually. Diagnostics and platform companies like Tempus ($1.27 billion in 2025 revenue) are demonstrating that AI-native healthcare companies can reach massive scale.

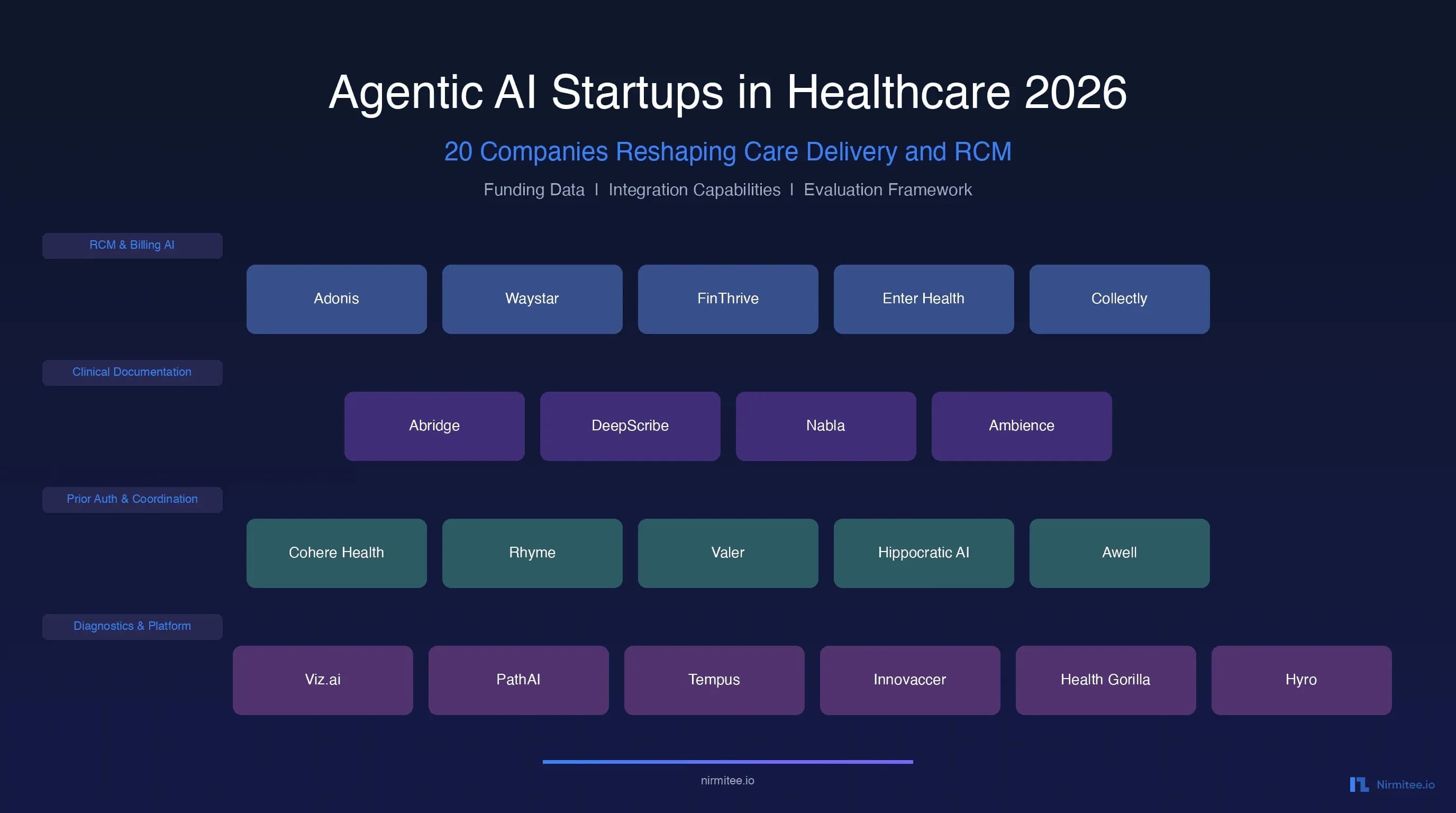

RCM and Billing AI: The Revenue Cycle Transformation

Revenue cycle management is the largest addressable market for healthcare AI. Medical documentation and back-office RCM combined account for 60% of healthcare IT spend, creating a $38 billion opportunity. These five companies are leading the charge with agentic AI that moves beyond simple automation into autonomous decision-making.

1. Adonis Health

What they do: AI-native RCM intelligence platform that layers on top of existing EHR and billing systems. Their AI agents analyze claims, payer behavior, and denial patterns to prevent revenue leakage before it happens.

- Founded: 2022 | Total Funding: $54 million (Series B led by Point72 Private Investments, June 2024)

- Key Metric: 4x revenue growth in 2025. Net revenue retention exceeding 130%. Processed over 100 million claims in 2024. 67% denial reduction for ApolloMD, 4.5x ROI in year one for Allied Digestive Health.

- Integration: REST APIs and webhooks. Connects to Epic, athenahealth, and NextGen. Partial FHIR R4. HL7 v2 limited (integrates at application layer, not interface engine level).

- Who it is for: Mid-to-large provider groups wanting AI-first denial prevention without replacing their EHR or PM system. Outcome-based pricing aligns incentives.

2. Waystar

What they do: End-to-end RCM platform with AltitudeAI powering financial clearance, claim management, and denial prevention. Public company (NYSE: WAY) that has become the 800-pound gorilla of RCM through strategic acquisitions.

- Founded: 2017 (via merger) | Revenue: $1.1 billion in 2025, guiding $1.27-$1.29 billion for 2026 (24% Q4 YoY growth)

- Key Metric: $15.5 billion in prevented denials in 2025. 50% of solutions now leverage AI. Serves 60% of the U.S. patient population.

- Integration: Strong FHIR R4, comprehensive HL7 v2, full X12 EDI. REST APIs available across product lines. Connects to all major EHRs.

- Best fit: Large health systems and hospitals needing enterprise-grade, end-to-end RCM with proven AI at scale.

3. FinThrive

What they do: Revenue integrity platform combining CDM management, charge capture, A/R optimization, and insurance discovery. Four-time KLAS "Best in KLAS" winner for Insurance Discovery. Their Fusion AI platform detects patterns across the revenue cycle.

- Founded: 2021 (rebrand of TransUnion Healthcare / Connance)

- Key Metric: Industry-leading insurance discovery. HITRUST CSF and SOC 2 certified. Processes billions in net patient revenue annually.

- Integration: Mature HL7 v2 and EDI. FHIR support partial and growing. REST APIs for core workflows.

- Built for: Revenue integrity-focused health systems wanting to capture missed charges and optimize payer contracts.

4. Enter Health

What they do: 100% API-driven RCM platform that automates from EMR to bank deposit. CTRL ENTER is a HIPAA-compliant AI desktop assistant for billing teams that prevents errors at the point of data entry.

- Founded: 2019 | Funding: Private

- Key Metric: Claims 98.5% of contract value collected. 15.5-day cash conversion cycle. SOC 2 Type II certified. Zero PHI used for model training.

- Integration: REST APIs and webhooks are first-class. X12 EDI for claims. FHIR partial. Strong clearinghouse connectivity.

- Aimed at: Practices frustrated with expensive native EHR billing that want modern, API-first RCM automation.

5. Collectly

What they do: AI-powered patient financial engagement platform with Billie, an AI voice agent for patient billing and RCM available 24/7 across chat, email, text, and voice.

- Started: 2019 | Total Funding: $34.1 million (Series A led by Sapphire Ventures). YC-backed.

- Key Metric: Launched Billie AI Eligibility and Benefits in October 2025 for automated real-time copay calculation and collection.

- Integration: EHR integrations for patient data sync. REST APIs. HIPAA-compliant across all channels.

- Strongest fit: Medical groups wanting to transform patient billing into a self-service, AI-driven experience that collects more while reducing staff burden.

Clinical Documentation: The Ambient AI Revolution

Clinical documentation is where healthcare AI has delivered the most dramatic, measurable impact. Healthcare AI spending in this category hit $600 million in 2025, growing 2.4x year-over-year. These four companies are eliminating the documentation burden that consumes up to 50% of a physician's day.

6. Abridge

What they do: Ambient AI clinical documentation platform that listens to patient-clinician conversations and generates structured clinical notes in the EHR. Now expanding beyond documentation into clinical workflow automation.

- Founded: 2018 | Total Funding: $800 million+ ($150M Series C, $250M Series D at $2.8B valuation, $300M Series E led by a16z at $5.3B valuation)

- Key Metric: The highest-funded ambient AI company in healthcare. Deployed across major health systems including UPMC, Yale New Haven, UCI Health.

- Integration: Deep EHR integration with Epic (Showroom listing), Oracle Health, MEDITECH. FHIR R4 for data exchange. SMART on FHIR for authentication.

- Ideal buyer: Health systems seeking the market leader in ambient documentation with the deepest EHR integration and the broadest specialty coverage.

7. DeepScribe

What they do: AI medical scribe built specifically for specialty care. Uses ambient intelligence to capture the full clinical encounter and generate specialty-specific documentation.

- Founded: 2017 | Total Funding: $60 million+

- Key Metric: 98.8 overall performance score from KLAS Research (early 2025). Ochsner Health selected DeepScribe for 4,700 clinicians. Partnership with Pearl Health for 3,500+ primary care providers. Partnership with Flatiron Health for oncology-focused ambient AI.

- Integration: EHR integrations for major platforms. REST APIs. Specialty-specific note templates.

- Customer profile: Specialty practices (orthopedics, cardiology, oncology) needing ambient AI purpose-built for their clinical vocabulary and workflow patterns.

8. Nabla

What they do: Agentic AI platform for clinical workflows that started with ambient documentation and is expanding into CDI, EHR action initiation, and cross-setting care support.

- Founded: 2018 (Paris, France) | Total Funding: $120 million (Series C of $70M led by HV Capital, June 2025)

- Key Metric: 5x revenue growth in 6 months. 85,000 clinicians and 20 million annual encounters. Peer-reviewed studies from the University of Iowa Health Care and Denver Health confirm documentation time cut by more than half and a 15-point increase in patient satisfaction.

- Integration: Epic, Oracle Health, athenahealth integrations. FHIR R4 support. REST APIs.

- Best fit: Health systems wanting ambient AI that extends beyond documentation into agentic clinical workflows, with strong clinical evidence backing.

9. Ambience Healthcare

What they do: End-to-end AI platform for documentation, coding, and clinical workflow support across the full continuum of care. Supports 100+ ambulatory subspecialties, EDs, and inpatient specialties.

- Founded: 2020 | Total Funding: $345 million ($243M Series C co-led by Oak HC/FT and a16z, July 2025, at $1.25B valuation)

- Key Metric: Achieved unicorn status. Part of Epic's Toolbox program. OpenAI Startup Fund investor. Covers the broadest range of specialties among ambient AI companies.

- Integration: Epic Toolbox integration (deep EHR embedding). Supports 100+ specialties, including inpatient and ED workflows. FHIR R4 support.

- Built for: Large health systems needing ambient AI that works across inpatient, outpatient, and emergency settings, not just primary care.

Prior Authorization: Eliminating the Biggest Administrative Bottleneck

Prior authorization consumes an estimated $31 billion annually in administrative costs across the U.S. healthcare system. CMS finalized rules requiring electronic prior authorization for Medicare Advantage and Medicaid by 2026, creating a regulatory tailwind for AI-powered solutions. These three companies are attacking the problem from different angles.

10. Cohere Health

What they do: AI-powered prior authorization and clinical decision-making platform for health plans. Their Cohere Unify platform uses intelligent prior authorization and payment integrity to reduce unnecessary burden while maintaining clinical quality.

- Launched: 2019 | Total Funding: $200 million ($90M Series C led by Temasek, May 2025)

- Key Metric: Processes 12 million+ prior authorization requests annually for 600,000+ providers. TIME World's Top HealthTech Companies 2025. Inc. 5000 list. Acquired ZignaAI (September 2025) for payment integrity expansion.

- Integration: Multi-payer platform with FHIR R4 and HL7 support. REST APIs and webhooks. Connects with major EHR and practice management systems.

- Aimed at: Health plans wanting to transform utilization management with AI that balances cost control and clinical quality. Also serves large provider organizations.

11. Rhyme Health

What they do: EHR-integrated prior authorization platform (formerly PriorAuthNow) that enables automated touchless processing of prior authorizations for both providers and payers.

- Founded: 2016 | Total Funding: ~$58 million (Series C, investors include Insight Partners, BIP Ventures, Health2047)

- Key Metric: Partners with 300+ health plans and 50 of the largest health systems. Processes 4 million+ authorization cases per year. KLAS Points of Light winner 2023 and 2024.

- Integration: Deep EHR integration is core to the product. Works with major payer platforms. Real-time authorization status tracking.

- Strongest fit: Health systems and large practices that want prior authorization automation embedded directly into their EHR workflow, with strong payer connectivity.

12. Valer

What they do: Cloud-based prior authorization and referral management platform that replaces individual payer portals with a single submission interface. Pre-populates payer forms with patient and insurance data from the EHR.

- Founded: 2015 | Funding: Private

- Key Metric: Slashes manual processing time by up to 75%. Partners include USC Keck, Kern Medical, OHSU, Golden Valley Health Centers, and Covenant Physician Partners. Covers all service types: professional, facility, technical, pharmacy, DME.

- Integration: EHR-integrated with automated data extraction. Single portal replacing multiple payer web and fax portals. Real-time payer status monitoring.

- Ideal buyer: Hospitals and mid-to-large physician practices that want to eliminate the multi-portal chaos of prior authorization without a massive implementation project.

Care Coordination: AI Agents for the Patient Journey

Care coordination is where agentic AI's ability to autonomously navigate complex, multi-step workflows truly shines. Unlike documentation AI (which observes and transcribes) or RCM AI (which processes claims), care coordination AI must reason about patient needs, clinical protocols, scheduling constraints, and payer requirements simultaneously.

13. Hippocratic AI

What they do: Safety-focused generative AI agents for patient-facing healthcare interactions. Their AI agents handle care coordination, chronic care management, post-discharge follow-up, and patient navigation tasks that currently fall on overwhelmed nursing staff.

- Founded: 2023 | Total Funding: $404 million ($126M Series C led by Avenir Growth at $3.5B valuation, November 2025)

- Key Metric: 115 million+ clinical patient interactions with zero reported safety issues. Partnerships with 50+ large health systems, payors, and pharmaceutical companies in six countries. Backed by Google CapitalG, a16z, and Kleiner Perkins.

- Integration: Multi-system integration capabilities. Supports FHIR R4 and REST APIs. Designed for compliance with clinical safety standards.

- Serves: Health systems and payors needing AI agents for patient communication tasks that require clinical safety guardrails, like post-discharge calls, care gap closure, and chronic disease management.

14. Awell Health

What they do: Care orchestration platform that enables healthcare organizations to design, automate, and optimize clinical pathways. Recently introduced agentic care flows that combine rules-based logic with LLM reasoning.

- Founded: 2018 (Gent, Belgium) | Total Funding: ~$9 million (Seed rounds from Octopus Ventures, LocalGlobe)

- Key Metric: Agentic care flows move from static rules to dynamic, context-aware clinical workflows. Open platform design allows custom care pathway creation without engineering resources.

- Integration: FHIR R4 native. REST APIs. Designed to orchestrate across multiple clinical systems. Cloud-based with webhook support.

- Best fit: Healthcare organizations that want to build and iterate on clinical pathways rapidly, with AI-augmented care flow orchestration, especially value-based care programs.

Patient Communication: AI-Powered Access and Engagement

Patient communication is where AI agents are having the most visible impact on the patient experience. Agentic AI is transforming healthcare workflows by resolving routine patient interactions autonomously, from scheduling to prescription management to billing inquiries.

15. Hyro

What they do: AI agents for healthcare that handle voice and digital patient interactions. Their hybrid architecture combines LLMs with proprietary small language models and knowledge graphs purpose-built for healthcare.

- Founded: 2018 | Total Funding: $95 million ($45M growth round led by Healthier Capital, October 2025, doubling valuation)

- Key Metric: Deployed at 45+ leading health systems, including Sutter Health, Tampa General Hospital, Prisma Health, and Piedmont Healthcare. Resolves up to 85% of routine patient interactions. Strategic investment from Bon Secours Mercy Health and ServiceNow Ventures.

- Connects to: Epic, Oracle Health, Salesforce integrations. HIPAA-compliant across all channels. Knowledge graph architecture adapts to each health system's specific services and protocols.

- Built for: Health systems wanting to automate call center volume (scheduling, routing, registration, prescription management) with AI that maintains clinical accuracy and HIPAA compliance.

16. Luma Health

What they do: Operational AI platform for healthcare that orchestrates front- and back-end workflows across the patient journey, from patient acquisition through scheduling, intake, and follow-up.

- Started: 2015 | Total Funding: $160 million (Series C)

- Key Metric: Saved 2 million+ hours of staff time in 2025. Deployed at 50+ health systems. Acquired Tonic Health from R1 (November 2025) to expand AI-driven patient intake and consent management, especially for Oracle Health EHR users.

- Works with: Epic, Oracle Health, athenahealth, NextGen integrations. FHIR R4 plus REST APIs and webhooks. Deep integration for scheduling, referral, and order orchestration.

- Aimed at: Health systems wanting operational AI that goes beyond point solutions (scheduling) into system-level workflow orchestration across the entire patient access journey.

Diagnostics and Clinical AI: AI at the Point of Decision

Diagnostic and clinical AI companies are different from the administrative AI companies above. They are making clinical decisions, not administrative ones, and that distinction matters enormously for regulatory requirements, liability, and integration depth.

17. Viz.ai

What they do: AI-powered care coordination platform that started with stroke detection and has expanded to cardiology, pulmonary embolism, aortic disease, and trauma. Their AI analyzes medical imaging in real-time and alerts the right specialist within minutes.

- Started: 2016 | Total Funding: $289 million ($100M Series D at $1.2B valuation)

- Key Metric: Deployed in 1,800+ hospitals. Life sciences business doubled over 18 months with 13 strategic pharmaceutical and medical device partnerships. Multiple FDA clearances. Systematic review and meta-analysis confirm significant improvement in stroke treatment times.

- Integration: Deep PACS and imaging system integration. HL7 v2 for ADT and order messages. FHIR R4 is supported, and it integrates with hospital communication systems for real-time specialist alerts.

- Strongest fit: Hospitals and health systems wanting AI-powered triage for time-sensitive conditions where minutes matter, particularly stroke, PE, and cardiac emergencies.

18. PathAI

What they do: AI-powered pathology platform transforming how diseases are diagnosed at the tissue level. Their AISight Dx platform enables digital pathology workflows across anatomic pathology labs.

- Launched: 2016 | Total Funding: $490 million ($165M Series C led by Kaiser Permanente)

- Key Metric: FDA breakthrough device designation for PathAssist Derm (AI-powered dermatopathology). 510(k) clearance for AISight Dx. Labcorp expanded its partnership (February 2026) to roll out digital pathology across US labs and hospital sites.

- Integration: LIS (Laboratory Information System) integration. DICOM for imaging data. REST APIs for workflow automation. HL7 for lab result messaging.

- Ideal buyer: Pathology labs, academic medical centers, and pharmaceutical companies needing AI-augmented diagnostic accuracy, especially in oncology and dermatopathology.

19. Tempus

What they do: AI-enabled precision medicine platform combining genomic sequencing, clinical data, and machine learning to personalize treatment decisions. Publicly traded (NASDAQ: TEM).

- Launched: 2015 | Revenue: $1.27 billion for 2025 (83% YoY growth). Guiding $1.59 billion for 2026 (25% growth).

- Key Metric: Diagnostics revenue $955 million (111% YoY growth). Oncology volume growth 26%. Data licensing revenue is growing 38% YoY. Achieved positive adjusted EBITDA in Q3 2025.

- Integration: Connects with major academic medical centers and oncology practices. FHIR R4 for clinical data exchange. Genomic data APIs. HL7 for lab result integration.

- Target buyer: Oncologists, academic medical centers, and pharmaceutical companies wanting AI-powered precision medicine with the largest real-world clinical and molecular dataset in healthcare.

Platform and Infrastructure: The Connective Tissue

These companies do not deliver AI to end users directly. Instead, they provide the data infrastructure, interoperability layer, and platform capabilities that other AI applications need to function. For healthcare CTOs, these are often the most strategically important partnerships because they enable everything else.

20. Innovaccer

What they do: Healthcare Intelligence Cloud that unifies patient data across sources and powers AI applications for population health, care management, and value-based care. Adding AI copilots and agents for utilization management, prior authorization, clinical decision support, and contact center automation.

- Founded: 2014 | Total Funding: $675 million ($275M Series F in January 2025 at $3.45B valuation)

- Key Metric: Serves 6 of the top 10 health systems. 130+ healthcare organizations on the platform. 50% year-over-year revenue growth for five consecutive years. Investors include Kaiser Permanente, Banner Health, and Danaher Ventures.

- Integration: Native FHIR R4 and HL7 v2. Connects to all major EHRs and HIEs. Developer ecosystem on the platform. HITRUST and SOC 2 certified.

- Best fit: Health systems and payors needing a unified data platform as the foundation for AI applications, population health, and value-based care initiatives.

21. Health Gorilla (Bonus)

What they do: Health data network and interoperability platform designated as a Qualified Health Information Network (QHIN) under TEFCA. Provides secure, real-time access to deduplicated, AI-ready health data.

- Founded: 2014 | Total Funding: $80 million ($50M Series C led by SignalFire)

- Key Metric: Query volume has grown from 200,000 to 66 million per month since going live as a QHIN. One of the inaugural data network early adopters in the CMS-Aligned Network. Strategic partnership with Altera Digital Health to integrate into Sunrise EHR (June 2025).

- Integration: Native FHIR R4. TEFCA-enabled nationwide data exchange. REST APIs. HL7 v2 support. Connects to labs, pharmacies, HIEs, and clinical data sources across the U.S.

- Built for: Healthcare AI companies, health systems, and digital health startups that need reliable, standards-based access to clinical data from across the U.S. healthcare ecosystem.

The CTO Evaluation Framework: How to Actually Choose

Listing companies is easy. Choosing between them is hard. Here is the five-dimensional evaluation framework we use when advising healthcare organizations on AI vendor selection. Every company on this list should be evaluated across all five dimensions before you sign a contract.

Dimension 1: Clinical Validation

Does the company have peer-reviewed outcomes data? Not case studies on their marketing site, but independent validation. Abridge has published research from UPMC and multiple academic medical centers. Nabla has peer-reviewed data from the University of Iowa and Denver Health. Viz.ai has a systematic review and meta-analysis confirming treatment time improvements. Many others have marketing metrics but no independent clinical validation.

- Ask for: published studies, FDA clearances, KLAS scores, clinical safety incident history

- Red flag: if the only "evidence" is a customer testimonial or a vendor-produced ROI calculation

Dimension 2: Integration Depth

How deeply does the AI agent integrate with your existing systems? Surface-level API calls are different from deep EHR embedding. Ambience Healthcare is in Epic's Toolbox program. Abridge has a Showroom listing. Rhyme is EHR-integrated at the workflow level. Others operate as standalone applications that require context-switching.

- Ask for: the FHIR implementation guide (not a marketing page about FHIR compliance), supported EHR versions, write-back capabilities, and whether it works within the EHR UI or requires a separate application

- Red flag: if "integration" means screen scraping, manual CSV uploads, or copy-paste between windows

Dimension 3: Security and Compliance

SOC 2 Type II is the minimum. HITRUST CSF is increasingly expected for enterprise health system contracts. Ask about PHI data handling: does the vendor use your patient data to train their models? Enter Health explicitly states zero PHI used for model training. Others are less transparent.

- Ask for: SOC 2 report, BAA terms, data residency options, model training data policies, and incident response history

- Red flag: if the vendor cannot produce a SOC 2 report or clearly articulate their PHI data handling policy

Dimension 4: Scalability and ROI

What is the total cost of ownership, and what measurable outcomes should you expect? Companies with outcome-based pricing (like Adonis) demonstrate confidence in their results. Look for net revenue retention above 120%, which signals that existing customers are expanding their use of the platform.

- Ask for: implementation timeline (under 90 days is ideal), pricing model details, reference customers at your scale, and measurable outcome guarantees

- Red flag: if implementation takes more than 6 months or the vendor will not share reference customers

Dimension 5: Vendor Viability

In a market where 54% of digital health funding goes to AI companies, funding alone does not signal viability. Look at revenue growth trajectory, customer concentration risk, and whether the company has a path to profitability. Tempus has demonstrated this at $1.27 billion in revenue. Waystar is profitable and public. Younger companies like Adonis (4x growth) and Nabla (5x growth in 6 months) show strong momentum but are earlier in the journey.

- Ask for: total funding and implied runway, revenue growth rate, customer count and concentration, and whether strategic acquirers have shown interest

- Red flag: if the company has raised capital but cannot demonstrate revenue growth or has a customer base concentrated in fewer than 10 accounts

Build vs. Buy: The Strategic Decision

The evaluation framework helps you choose between vendors. But there is a prior question that many healthcare CTOs skip: should you build AI capabilities in-house, buy from a vendor, or take a hybrid approach?

The honest answer for most health systems in 2026: buy proven AI agents for well-defined use cases, build custom workflows on top. The companies on this list have invested $100-$800 million each in building their AI platforms. Replicating that investment in-house is unrealistic for all but the largest academic medical centers with dedicated AI research teams.

Where building makes sense: when AI is your core differentiator (you are building a health tech product), when you have unique data assets that create a defensible moat, or when the specific workflow you are automating is so organization-specific that no vendor solution fits.

Where buying makes sense: clinical documentation (Abridge, Nabla, Ambience), prior authorization (Cohere, Rhyme), patient communication (Hyro, Luma Health), and RCM augmentation (Adonis, Collectly). These are well-defined problem spaces where vendor solutions have demonstrated measurable ROI and the cost of building internally far exceeds the cost of licensing.

Market Trends

Consolidation is accelerating. Luma Health acquired Tonic Health. Cohere Health acquired ZignaAI. Expect larger players (Waystar, Innovaccer, the EHR vendors) to acquire successful point solutions to build end-to-end platforms.

Clinical documentation companies are expanding into RCM. Abridge, Nabla, and Ambience all started with ambient documentation. Now they are moving into coding, CDI, and billing workflow automation. The boundary between "documentation AI" and "RCM AI" is blurring.

Regulatory tailwinds are strong. CMS electronic prior authorization rules (effective 2026), ONC information blocking enforcement, and TEFCA adoption are all pushing healthcare toward the standardized, digital workflows that AI companies need to operate effectively.

Agentic AI is moving from demos to production. The 2025 hype cycle for agentic AI is giving way to real deployments in 2026. Companies like Hippocratic AI (115 million patient interactions) and Hyro (85% resolution rate) are demonstrating that AI agents can operate autonomously at scale in healthcare without safety incidents.

If you are evaluating any of the companies on this list for integration with your healthcare AI solutions, the most important thing is to move beyond the funding headlines and marketing claims. Ask for the clinical evidence, test the integration depth, and verify the ROI with reference customers who look like you.