Choosing a revenue cycle management partner is one of the highest-stakes decisions a healthcare organization makes. Get it right, and you unlock millions in recovered revenue, faster reimbursements, and a finance team that can actually focus on strategy. Get it wrong, and you're locked into a multi-year contract with rising denial rates, opaque reporting, and a vendor that treats your account like a number.

The strategic destination all these vendors are racing toward is the touchless revenue cycle described in McKinsey's framework.

The problem with most "top RCM companies" lists is that they're vendor directories, not practitioner reviews. They list features without context, skip the uncomfortable truths about contract structures, and never tell you which companies consistently under-deliver after the sales demo.

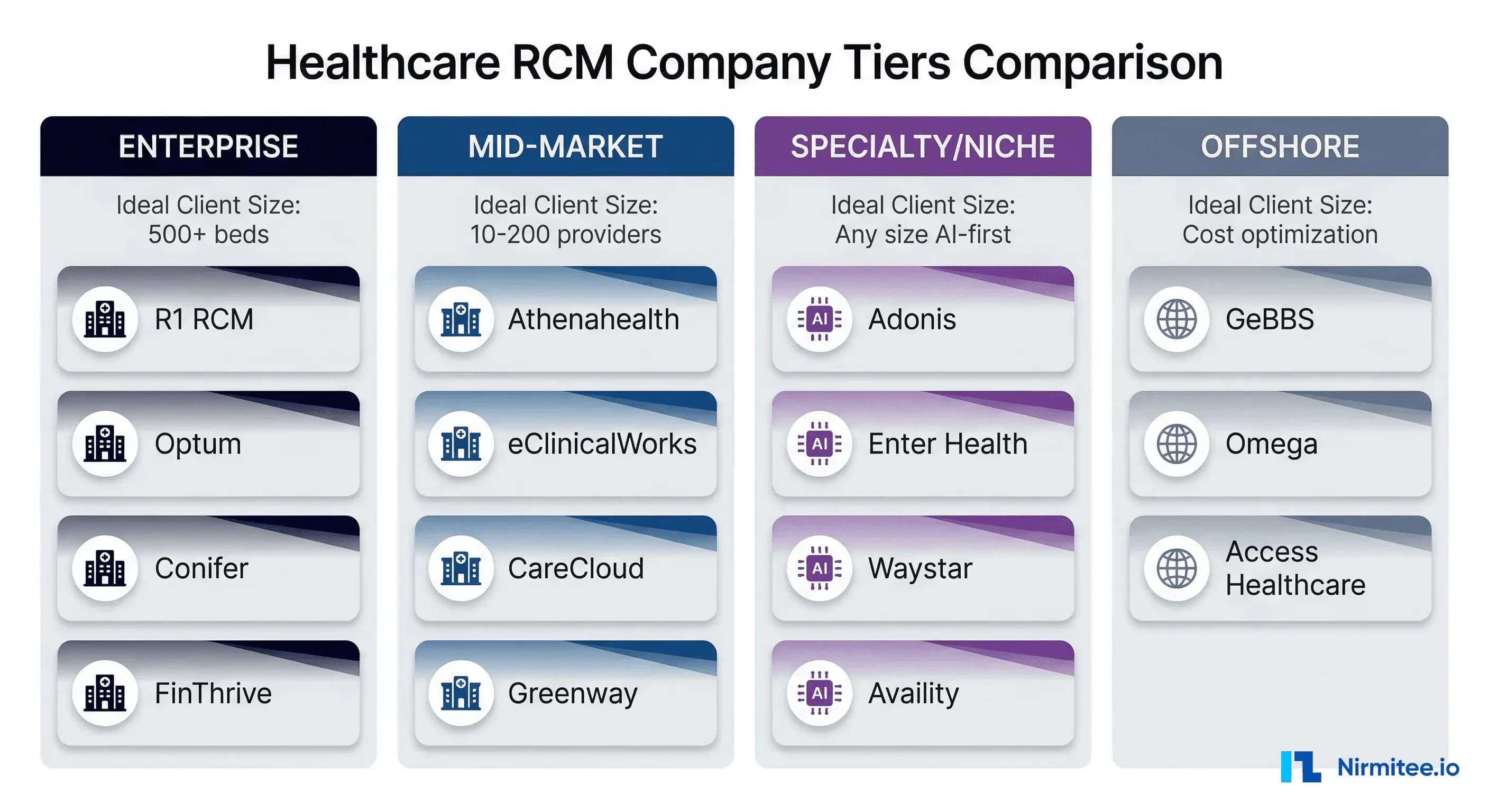

This guide is different. We've organized 15 RCM companies into four tiers based on ideal client fit, evaluated their real-world strengths and weaknesses, and added the selection criteria, red flags, and negotiation tactics that most reviews conveniently omit. Whether you're a 500-bed health system evaluating enterprise partners or a 20-provider group looking for your first outsourced RCM solution, this is the practitioner's guide to making that decision.

The 2026 RCM Market: What's Actually Changed

The global revenue cycle management market reached approximately $181 billion in 2026, growing at a 12.7% CAGR projected through 2034, according to Fortune Business Insights. The U.S. alone accounts for roughly $73 billion of that market. But the numbers don't tell the full story.

Three structural shifts are reshaping how organizations should evaluate RCM partners in 2026:

1. Denial rates are the new crisis. According to the Adonis 2026 RCM Report, external payer dynamics — particularly denials and reimbursement pressure — have surpassed staffing and operational inefficiencies as the primary threats to revenue performance. Average denial rates across the industry sit between 10% and 15%, with top-performing organizations targeting under 5%.

2. Vendor consolidation is accelerating. A FinThrive 2026 report found that nearly 60% of health systems plan to consolidate RCM vendors within the next three years, and over 70% expect to reduce reliance on third-party vendors entirely. If your current vendor isn't investing in platform breadth, they may not survive the consolidation wave.

3. AI moved from buzzword to differentiator. Waystar was rated #1 overall in Black Book's Q1 2026 Agentic and Generative AI RCM Benchmark, and 66% of organizations identified "automated denial follow-up and resolution" as a "very important" AI capability for their 2026 RCM strategy. Vendors without credible AI strategies are falling behind measurably.

With that context, here's how the 15 most significant RCM companies stack up — organized by the type of organization they actually serve well.

Tier 1: Enterprise RCM (Health Systems, 500+ Beds)

Enterprise RCM is a different category entirely. These vendors manage billions in net patient revenue, embed teams on-site, and typically require multi-year commitments. The upside is comprehensive support; the downside is switching costs that can paralyze an organization for years.

R1 RCM

What they do: End-to-end revenue cycle operations for hospitals, health systems, and large physician groups. R1 manages the full spectrum from pre-registration and charge capture through coding, billing, denials management, and underpayment recovery. They process over $30 billion in annual net patient revenue.

Strengths: R1 earned multiple "Best in KLAS" awards in 2025. Their operating model embeds dedicated teams within client organizations, creating deep institutional knowledge. Their recent partnership with AI scribe Heidi to integrate clinical documentation directly into R1's revenue operating system signals serious investment in the clinical-financial data bridge.

Weaknesses: R1's model works best at scale — smaller health systems (under 300 beds) often report feeling like secondary priorities. Implementation timelines can stretch 6-9 months. The embedded team model creates significant vendor lock-in; transitioning away from R1 is notoriously disruptive.

Ideal client: Multi-hospital health systems with $500M+ in net patient revenue seeking a single partner to own the entire revenue cycle.

Contract model: Typically percentage-of-collections (4-7%) with performance guarantees and multi-year terms (3-5 years).

Integration: Strong HL7v2 and EDI support. FHIR capabilities are developing but are not a primary differentiator. Deep integrations with Epic, Cerner/Oracle Health, and Meditech.

Optum / Change Healthcare

What they do: Optum combines technology, payer insights, and operational expertise across coding, billing, analytics, and workflow management. Their acquisition of Change Healthcare created the largest healthcare data and analytics company in the U.S.

Strengths: Unmatched payer data access through UnitedHealth Group ownership — no other RCM vendor can offer the same level of insight into payer behavior and adjudication patterns. The May 2025 launch of Optum Integrity One, an AI-powered integrated revenue cycle platform, positions them at the forefront of AI-driven RCM. Excellent for large-scale financial forecasting.

Weaknesses: The UnitedHealth Group connection is a double-edged sword. Many provider organizations are uncomfortable giving revenue cycle data to a company owned by the nation's largest payer. Post-Change Healthcare merger integration continues to create service disruptions for some clients. The 2024 Change Healthcare cyberattack still lingers in institutional memory.

Ideal client: Large health systems that prioritize data-driven optimization and are comfortable with the UHG relationship. Organizations already using Optum products (coding, analytics, clinical) get the most seamless integration.

Contract model: Variable — ranges from technology licensing (SaaS) to full outsourced operations. Enterprise deals are highly customized.

Integration: Comprehensive EDI/HL7/FHIR capabilities through Change Healthcare's clearinghouse network, which processes billions of transactions annually.

Conifer Health Solutions

What they do: Conifer is Tenet Healthcare's RCM subsidiary, managing over 17 million unique patient encounters annually across more than $32 billion in net patient revenue. In January 2026, Tenet regained full ownership of Conifer after CommonSpirit Health exited with a $1.9 billion contract termination payment.

Strengths: Conifer's partnership with Google Cloud for end-to-end AI RCM is one of the most ambitious technology plays in the industry. They bring genuine operational expertise from running Tenet's own revenue cycle. The CommonSpirit exit, while negative optically, actually gives Conifer more operational flexibility and a cleaner growth trajectory.

Weaknesses: Conifer's client base has historically been concentrated among Tenet-affiliated hospitals. Diversification is ongoing but not yet proven at scale for non-Tenet organizations. The CommonSpirit departure raised questions about client retention capability.

Ideal client: Large hospital systems seeking an established operator with serious AI investment and willingness to negotiate aggressively (given their need to prove non-Tenet market viability).

Contract model: Full outsource, typically percentage-of-collections with performance-based components.

Integration: Strong EHR integrations across major platforms. Google Cloud partnership enhances data analytics capabilities.

FinThrive (formerly nThrive)

What they do: FinThrive provides revenue cycle technology across patient access, charge integrity, claims management, and contract management. They position as a technology-first company rather than an outsourced services provider.

Strengths: FinThrive's 2026 Transformative Trends Report found that 71% of RCM leaders now prioritize patient experience over revenue — and FinThrive's platform is designed around this shift. Their charge integrity and contract management modules are genuinely best-in-class. A technology-forward approach means faster innovation cycles than traditional BPO-style vendors.

Weaknesses: FinThrive is a technology platform, not a fully outsourced service. Organizations expecting "hand it over and forget about it" will be disappointed — you need internal staff to operate the platform effectively. Pricing can be complex with multiple module licensing.

Ideal client: Health systems with capable internal revenue cycle teams that need better technology, not more bodies. Organizations focused on the patient financial experience.

Contract model: SaaS licensing by module, typically with implementation fees. Some performance-based components available.

Integration: Strong FHIR and HL7 support. Purpose-built integrations with Epic, Oracle Health, and MEDITECH.

Tier 2: Mid-Market RCM (10-200 Providers)

Mid-market RCM is where most organizations live — and where vendor selection matters most. Enterprise vendors won't give you attention at this scale, and niche vendors may lack the breadth you need. These four vendors are purpose-built for mid-market healthcare organizations.

Athenahealth

What they do: Cloud-based platform combining EHR, practice management, and full revenue cycle management in a unified system. Athenahealth consistently wins KLAS awards for integrated ambulatory platforms.

Strengths: The "services-enabled platform" model is Athenahealth's killer advantage. Customers consistently highlight the value of bundling software with RCM services as a "cohesive package." Best in KLAS 2025 for Independent Physician Practice. Their network effect — athenaNet — means billing rules and payer intelligence improve for everyone as the network grows. Scales from small practices to large enterprises.

Weaknesses: If you're not using Athena's EHR, the RCM capabilities are significantly diminished — this is a platform play, not a standalone RCM service. Pricing is percentage-based and can get expensive for high-revenue practices. Customization is limited compared to best-of-breed point solutions.

Ideal client: Ambulatory practices with 5-200 providers who want a single platform for EHR + RCM and are willing to adopt the Athena ecosystem entirely. Backed by Bain Capital and Hellman & Friedman.

Contract model: Percentage of collections (typically 4-8%) with multi-year terms. Includes EHR licensing.

Integration: Proprietary athenaNet network. API-based integrations are available, but the platform works best as a self-contained ecosystem.

eClinicalWorks RCM

What they do: eClinicalWorks claims the title of the largest cloud-based ambulatory EHR by installed base, with over 850,000 physicians on the platform. Their RCM services layer on top of the EHR for billing, coding, and claims management.

Strengths: A massive installed base means extensive payer rules and billing intelligence. Cost-competitive compared to Athenahealth. Strong in primary care and multi-specialty groups. If you're already on eCW's EHR, adding RCM is seamless.

Weaknesses: KLAS feedback consistently cites "missing functionality" and "immature solutions" as reasons clients look to third-party additions. The RCM service quality can vary significantly by region and account manager. The platform's strength is breadth, not depth — specialized billing scenarios may require workarounds.

Ideal client: Large ambulatory practices (10-100+ providers) already on the eCW EHR platform, particularly in primary care and general multi-specialty settings where billing complexity is moderate.

Contract model: Bundled with EHR licensing, percentage-based or per-encounter pricing. Generally more affordable than Athenahealth.

Integration: Tight integration within the eCW ecosystem. HL7 and basic FHIR support for external connections.

CareCloud

What they do: Cloud-native revenue cycle management designed specifically for small- to mid-size practices. Emphasizes ease of use, rapid implementation, and scalability.

Strengths: CareCloud's cloud-native architecture enables genuinely faster deployment than legacy competitors — weeks, not months. The platform is designed for practices that don't have dedicated billing departments. Clean, modern UI that billing staff actually want to use. Good analytics dashboard for practice managers without a data science background.

Weaknesses: Limited depth for complex enterprise scenarios. The integration ecosystem is smaller than Athena or eCW. Less proven track record with large multi-location groups. Customer support quality has been inconsistent in recent reviews.

Ideal client: Small to mid-size practices (1-50 providers) seeking a modern, easy-to-deploy cloud platform without the complexity of enterprise solutions. Organizations that value speed-to-value over feature completeness.

Contract model: SaaS subscription with optional RCM services add-on. Generally fixed monthly pricing.

Integration: REST API-based integrations. Supports HL7 and basic FHIR connectivity.

Greenway Health

What they do: Revenue cycle management built around an intelligent dashboard system providing a streamlined overview of financial performance. Backed by Vista Equity Partners.

Strengths: Strong practice management and financial analytics. Vista Equity ownership brings operational discipline and investment capital. Purpose-built for ambulatory settings with specialty-specific workflows for cardiology, orthopedics, and other high-revenue specialties.

Weaknesses: KLAS feedback consistently points to limitations in telehealth and virtual care billing — a critical gap given post-pandemic care delivery trends. The platform can feel dated compared to cloud-native competitors. Specialty workflows are a strength but also mean the platform is less flexible for general use cases.

Ideal client: Mid-size specialty practices (10-75 providers) that need specialty-specific billing workflows and strong financial reporting. Organizations are less focused on telehealth revenue.

Contract model: Subscription-based with implementation fees. RCM services are available as a managed add-on.

Integration: HL7v2 and EDI support. FHIR capabilities are in development but are not a current strength.

Tier 3: Specialty and AI-Native RCM

This tier includes the most interesting companies in the 2026 RCM landscape — vendors that are either AI-native, platform-first, or solving specific problems that traditional RCM companies haven't addressed. These aren't necessarily better or worse than Tier 1-2; they're different in fundamental architecture.

Adonis

What they do: AI-native revenue cycle management platform that identifies revenue risk early and automates resolution across denials, delays, and payer friction. Adonis closed 2025 with over 4x revenue growth and net revenue retention exceeding 130%.

Strengths: Purpose-built on AI from day one, not AI bolted onto legacy systems. The platform excels at predictive analytics — identifying claims likely to be denied before submission. Their 2026 RCM Report has become an industry-cited data source, establishing thought leadership. Rapid customer expansion across provider groups, hospitals, and health systems. Named to the 2026 DH100 by Digital Health New York.

Weaknesses: Relatively young company — long-term viability is unproven compared to R1 or Athenahealth. The platform is a technology layer, not a full-service outsourced operation. Organizations expecting white-glove managed services may find Adonis's self-service model insufficient. Best suited for organizations with some internal billing capability.

Ideal client: Forward-thinking provider organizations of any size that want AI-driven revenue intelligence and have internal staff to act on the insights. Health systems frustrated with legacy vendors' slow AI adoption.

Contract model: SaaS subscription, typically priced per provider or per encounter. No long-term lock-in contracts.

Integration: Modern API-first architecture with FHIR R4 support. Integrates with all major EHR platforms. Designed for interoperability from the ground up.

Enter Health

What they do: AI-first RCM solution focused on reducing claim denials and eliminating administrative burdens. Enter differentiates on implementation speed — full implementation in just 40 days, compared to 6-9 months for traditional vendors.

Strengths: The 40-day implementation timeline is genuinely disruptive. SOC 2 Type II certified and HIPAA compliant from day one. Designed specifically for practices that need to get operational fast without lengthy migration projects. Strong focus on claim denial reduction as a primary outcome metric.

Weaknesses: Limited track record with large enterprise health systems. The rapid implementation model may sacrifice some customization depth. A smaller customer base means less payer intelligence from network effects compared to Athenahealth or eCW.

Ideal client: Practices of any size that need to switch RCM vendors quickly — whether due to vendor failure, acquisition, or startup. Organizations that value speed-to-value and can't afford a 6-month migration timeline.

Contract model: Flexible terms without long-term lock-in. Pricing varies by practice size and complexity.

Integration: Built for modern EHR ecosystems. Strong Epic integration capabilities. FHIR-capable architecture.

Waystar

What they do: Revenue cycle technology platform spanning the full financial journey from patient access through payment. Waystar was rated #1 overall in Black Book's Q1 2026 Agentic and Generative AI RCM Benchmark across 20 qualifying vendors.

Strengths: The Black Book benchmark ranking across 18 KPIs is the most credible third-party AI validation any RCM vendor has received in 2026. Waystar's Agentic Readiness Index and Revenue Protection Score led the benchmark. Their platform covers the full pre-service through post-adjudication workflow. Strong clearinghouse capabilities with broad payer connectivity.

Weaknesses: Waystar is primarily a technology platform — organizations seeking fully managed RCM services need to pair it with internal staff or a separate services partner. Premium pricing reflects the technology investment. Some clients report a steep learning curve during initial deployment.

Ideal client: Health systems and large practices that want best-in-class RCM technology with genuine AI capabilities and have the internal team to leverage the platform. Organizations prioritizing claims denial management and payer intelligence.

Contract model: Enterprise SaaS licensing with implementation services. Transaction-based pricing for clearinghouse services.

Integration: Comprehensive EDI, HL7, and FHIR support. Deep EHR integrations across all major platforms. API-first architecture.

Availity

What they do: Healthcare intelligence network and revenue cycle platform connecting providers, payers, and patients. Availity's clearinghouse processes billions of transactions, making it one of the largest healthcare data networks in the U.S.

Strengths: Availity's core strength is payer connectivity — their network connects to virtually every commercial and government payer. Availity Essentials Pro provides integrated pre-service, post-service, and post-adjudication capabilities in a single platform. AI-powered predictive claim editing analyzes claims before payer submission, reducing back-end denials. Trusted by a massive provider base for reliability.

Weaknesses: Availity's strength is the network and clearinghouse, not full-service RCM operations. Organizations expecting end-to-end managed billing services need additional partners. The platform can feel transactional rather than strategic for organizations wanting deep analytics and consulting.

Ideal client: Provider organizations of any size that need reliable, broad payer connectivity and claims management. Works well as a clearinghouse/technology layer paired with in-house billing staff or a managed services partner.

Contract model: Tiered subscription. Essentials (free basic tier) through Essentials Pro (premium). Transaction-based pricing for claims volume.

Integration: Industry-leading EDI connectivity. HL7 and FHIR support. Designed as a hub connecting disparate systems across the provider-payer ecosystem.

Tier 4: Offshore RCM Partners

Offshore RCM is not a compromise — when done right, it's a strategic cost optimization that can deliver equivalent or better quality at 40-60% lower cost. The key is selecting vendors with U.S.-based oversight, HIPAA-compliant operations, and proven quality metrics. Here are the three dominant offshore RCM players.

GeBBS Healthcare Solutions

What they do: Global revenue cycle outsourcing across coding, billing, follow-up, and quality assurance. Founded in 2005 and headquartered in Culver City, California, GeBBS operates with approximately 11,000 employees across 11 global offices. Acquired by EQT in September 2024 at an $850M+ valuation.

Strengths: The EQT acquisition at $850M+ validates GeBBS as a premium coding and RCM outsourcing provider, not a budget operation. Their offshore delivery model allows providers to scale operations while managing costs. Strong quality assurance frameworks and U.S.-based client management. HITRUST CSF certified. Comprehensive service coverage from eligibility through A/R recovery.

Weaknesses: Offshore delivery means time zone challenges for real-time issue resolution. Cultural and communication gaps can impact complex denial resolution requiring nuanced payer negotiation. Dependency on offshore labor markets creates concentration risk. Post-acquisition integration may shift strategic priorities.

Ideal client: Health systems and large physician groups seeking significant cost reduction (40-50% savings) on coding and billing operations while maintaining quality through U.S.-based oversight. Organizations processing 50,000+ claims annually get the best economics.

Contract model: FTE-based pricing ($2,500-4,000/FTE/month) or per-transaction pricing. Hybrid models available. Typically 2-3 year terms.

Integration: Works with all major EHR and PMS platforms. EDI and HL7 capable. Integration depth depends on the specific service scope.

Omega Healthcare

What they do: Revenue cycle support, including coding, claims processing, and A/R management. Omega Healthcare won the 2026 Best in KLAS Award for Ambulatory RCM Services (EHR Agnostic) with an overall performance score of 92.2 — a remarkable achievement for an offshore-origin company.

Strengths: The 2026 Best in KLAS award is the strongest third-party validation any offshore RCM provider has received. EHR-agnostic approach means Omega works across any technology stack. The 92.2 KLAS score puts them ahead of many domestic competitors. Strong clinical quality with certified coders across multiple specialties.

Weaknesses: KLAS recognition may attract growth that strains service delivery capacity. Ambulatory focus means less proven capability for large hospital system revenue cycles. The "offshore" label still carries a stigma with some provider organizations regardless of actual quality metrics.

Ideal client: Ambulatory practices and physician groups of any size seeking best-in-class outsourced RCM without EHR platform lock-in. Organizations that evaluate on quality metrics rather than vendor origin.

Contract model: Flexible pricing models including per-transaction, FTE-based, and percentage-of-collections. Generally, more flexible terms than those of enterprise domestic vendors.

Integration: EHR-agnostic — certified integrations across Epic, Cerner/Oracle, Allscripts, eCW, Athena, and others. EDI and HL7 support.

Access Healthcare

What they do: Large-scale healthcare BPO and RCM outsourcing with comprehensive service coverage from front-end patient access through back-end A/R management. Access Healthcare secured $211 million in funding in January 2025, signaling serious growth ambitions.

Strengths: The $211M funding round provides capital for technology investment and expansion that most offshore competitors lack. Comprehensive service coverage across the entire revenue cycle. Strong in high-volume, process-driven RCM functions. Competitive pricing with scale economies.

Weaknesses: Less brand recognition than GeBBS or Omega in the U.S. market. Quality consistency across a rapidly scaling operation is an ongoing challenge. The technology platform is less differentiated than AI-native competitors. Growth phase means organizational maturity is still developing.

Ideal client: Large health systems and physician groups processing high claim volumes that need significant cost reduction through offshore delivery. Organizations with existing internal RCM infrastructure that need augmentation rather than replacement.

Contract model: FTE-based and transaction-based pricing. Competitive rates reflecting scale economies. Flexible terms for large-volume engagements.

Integration: Works across all major EHR platforms. EDI and HL7 standard integrations. API capabilities developing.

10 Red Flags When Evaluating RCM Vendors

Before you sign anything, run your prospective RCM partner through these red flags. Any single flag warrants deeper investigation; three or more should disqualify the vendor.

1. No transparent pricing breakdown. If a vendor can't clearly articulate what you're paying for — base fees, transaction fees, implementation costs, termination fees — they're hiding something. Demand a complete fee schedule before any contract discussion.

2. Reports claims submitted, not claims paid. This is the most common metric manipulation in RCM. A vendor that touts a "99% clean claim rate" but can't tell you their first-pass resolution rate (claims paid without rework) is measuring activity, not outcomes.

3. Refuses to share denial rate benchmarks. Every credible RCM vendor tracks denial rates by payer, by denial reason code, and by service line. If they can't (or won't) share these benchmarks during the evaluation, they either don't track them or don't want you to see the numbers.

4. Long-term lock-in with no performance guarantees. A 3-5 year contract isn't inherently bad — but a 3-5 year contract without performance-based exit clauses is. Insist on contractual KPIs with remediation timelines and termination rights if benchmarks aren't met.

5. Cannot segment denial data by root cause. "Your denial rate is 8%" is useless without knowing why. Is it eligibility denials? Prior authorization failures? Coding errors? Medical necessity? A vendor that can't segment denial data by root cause can't systematically reduce denials.

6. No FHIR or HL7 integration capability. It's 2026. If a vendor's integration strategy is still based entirely on CSV file drops and manual data entry, they're not investing in technology. Modern RCM platforms should support HL7v2 at minimum and ideally FHIR R4 for real-time data exchange.

7. Offshore team with no U.S.-based oversight. Offshore delivery isn't a red flag — lack of U.S.-based oversight is. Your RCM partner should have domestic account managers, quality assurance, and escalation paths regardless of where the operational team sits.

8. Single-payer dependency over 40%. If a vendor's revenue cycle expertise is concentrated in a single payer (e.g., they primarily serve Medicare-heavy practices), they may lack the breadth to handle your commercial payer mix effectively.

9. Implementation timeline exceeds 6 months. For mid-market practices, a full RCM implementation should take 8-16 weeks. If a vendor quotes 6+ months for a practice under 100 providers, they either lack implementation resources or their technology requires excessive customization.

10. No SOC 2 Type II or HITRUST certification. In 2026, these aren't nice-to-haves — they're table stakes. If a vendor handling your patient financial data can't demonstrate SOC 2 Type II compliance at minimum, walk away. HITRUST is increasingly expected for healthcare-specific engagements.

Contract Negotiation Tips That Save Real Money

Most healthcare organizations leave significant value on the table during RCM contract negotiations because they don't know what's negotiable. Here's what experienced revenue cycle leaders negotiate:

Performance-based fee structures. The best RCM contracts include performance-based components — the vendor earns bonuses for exceeding KPI targets and provides credits when they fall short. According to HealthLeaders Media, performance-based terms should include specific remediation timelines and client termination rights for repeated failures.

Carve out denial rate guarantees. Negotiate a maximum denial rate threshold (e.g., under 5% first-pass denial rate) with financial consequences if exceeded. This single clause changes vendor behavior more than any other contractual mechanism.

Data ownership and portability. Explicitly define in the contract that all claim data, denial analytics, payer intelligence, and operational reports are your property and must be provided in standard formats (CSV, HL7, FHIR) upon contract termination with no additional fees.

Transition support obligations. Require 90-day transition support at no additional cost when the contract ends — whether by expiration or termination. This prevents vendors from holding your revenue cycle hostage during transitions.

Avoid auto-renewal traps. Many RCM contracts auto-renew for 1-2 year terms with 90-180 day notice requirements. Negotiate down to 30-day notice and annual (not multi-year) auto-renewal terms.

Cap price escalation. Annual price increases should be capped at CPI or a fixed percentage (3-4%), not left to vendor discretion. Uncapped escalation clauses are the single biggest source of RCM cost creep.

Implementation Timeline: What to Actually Expect

Vendors will tell you what you want to hear during the sales process. Here's what actually happens during RCM implementation, based on real-world timelines:

Weeks 1-2: Discovery and Assessment. Workflow audit, current state documentation, data migration planning, and team introductions. This phase is often rushed by vendors eager to show progress — push back and insist on thorough discovery. Poor discovery leads to poor implementation.

Weeks 3-4: Integration Setup. EHR/PMS connection, EDI enrollment with payers, clearinghouse configuration, and user account provisioning. This is where integration capability separates good vendors from bad ones. If your vendor is still doing manual EDI enrollment in 2026, expect delays.

Weeks 5-8: Parallel Processing. Run both old and new systems simultaneously. This is the most expensive and painful phase but also the most important. Never let a vendor skip parallel processing — it's your safety net for catching billing errors before they hit your revenue.

Weeks 9-12: Full Go-Live. Cutover to the new system, intensive staff training, and active monitoring. Expect a temporary dip in collections (15-20%) during the first 30 days of go-live. If a vendor promises no disruption during cutover, they're lying.

Ongoing: Optimization. KPI tracking, denial pattern analysis, process tuning, and quarterly business reviews. The first 90 days post-go-live are critical — insist on weekly performance reviews during this period.

Realistic timelines by organization size:

- Small practice (1-10 providers): 6-10 weeks

- Mid-market (10-100 providers): 10-16 weeks

- Enterprise (100+ providers/health system): 16-24 weeks

- AI-native vendors (Adonis, Enter Health): 4-8 weeks

Build In-House vs. Outsource: The Decision Framework

Not every organization should outsource RCM. And not every organization should build in-house. Here's a structured framework for making that decision:

Build In-House When:

- Annual net patient revenue exceeds $50M and you can justify 5+ dedicated billing FTEs

- Your specialty has unique billing complexity (behavioral health, substance abuse, complex surgical) that generic vendors handle poorly

- You have access to experienced billing talent in your market

- Data control is a strategic priority — you want to own your revenue intelligence entirely

- You're willing to invest in technology — AI-powered RCM platforms like those powering custom RCM software development can make small teams highly productive

Expected cost: $8-15 per claim (fully loaded, including technology, staff, training, and overhead)

Outsource When:

- Annual net patient revenue is under $20M and you can't justify dedicated billing staff

- Your billing is straightforward — primary care, general internal medicine, standard surgical

- You're in a tight labor market and can't recruit or retain billing talent

- You're growing rapidly and need billing capacity to scale without hiring delays

- You want predictable costs — percentage-of-collections models align vendor incentives with your revenue

Expected cost: 4-8% of net collections (outsourced) or $3-8 per claim (transaction-based)

Hybrid Model When:

- Revenue is $20-50M — large enough for some internal capability but not fully in-house

- You want to keep strategic functions in-house (denial management, payer negotiations) while outsourcing routine processing

- You're transitioning from outsourced to in-house (or vice versa) and need a bridge

Expected cost: $5-10 per claim blended, with internal team handling high-value functions

How to Make Your Final Decision

After evaluating vendors against these tiers, red flags, and criteria, here's the decision process that works:

- Define your tier. Be honest about your organization's size, complexity, and internal capabilities. Don't evaluate enterprise vendors if you're mid-market.

- Shortlist 3 vendors maximum. More than three creates evaluation fatigue and delays decisions. Pick the best fit from your tier plus one stretch option.

- Request a proof of concept, not a demo. Demos show the best-case scenario. Ask each vendor to process 100-200 real claims from your current A/R and measure actual outcomes.

- Check references at a similar scale. Don't accept references from clients 10x your size. Ask for references from organizations within 20% of your provider count and revenue.

- Negotiate the contract last. Select your preferred vendor on capability and fit first, then negotiate terms. Negotiating with multiple vendors simultaneously wastes everyone's time and creates adversarial relationships.

The RCM vendor landscape in 2026 offers more options than ever — from AI-native platforms that implement in weeks to enterprise partners managing billions in revenue. The organizations that succeed are the ones that match their actual needs to the right tier, ask the uncomfortable questions during evaluation, and negotiate contracts that protect their interests for the long term.