A CTO at a 6-hospital system told me in January that she had 23 vendor demos scheduled in Q1 alone—all claiming to be "the AI agent platform for healthcare." She cancelled 19 of them after the third vendor could not explain how their product differed from a chatbot with a HIPAA BAA.

The agentic AI vendor landscape in healthcare has exploded. Hippocratic AI raised $126M at a $3.5B valuation. Hyro closed $45M to scale patient communication agents. Waystar was rated #1 in Black Book's Q1 2026 Agentic AI RCM benchmark. Meanwhile, YC-backed startups like Paratus Health are automating entire clinic front desks in three weeks.

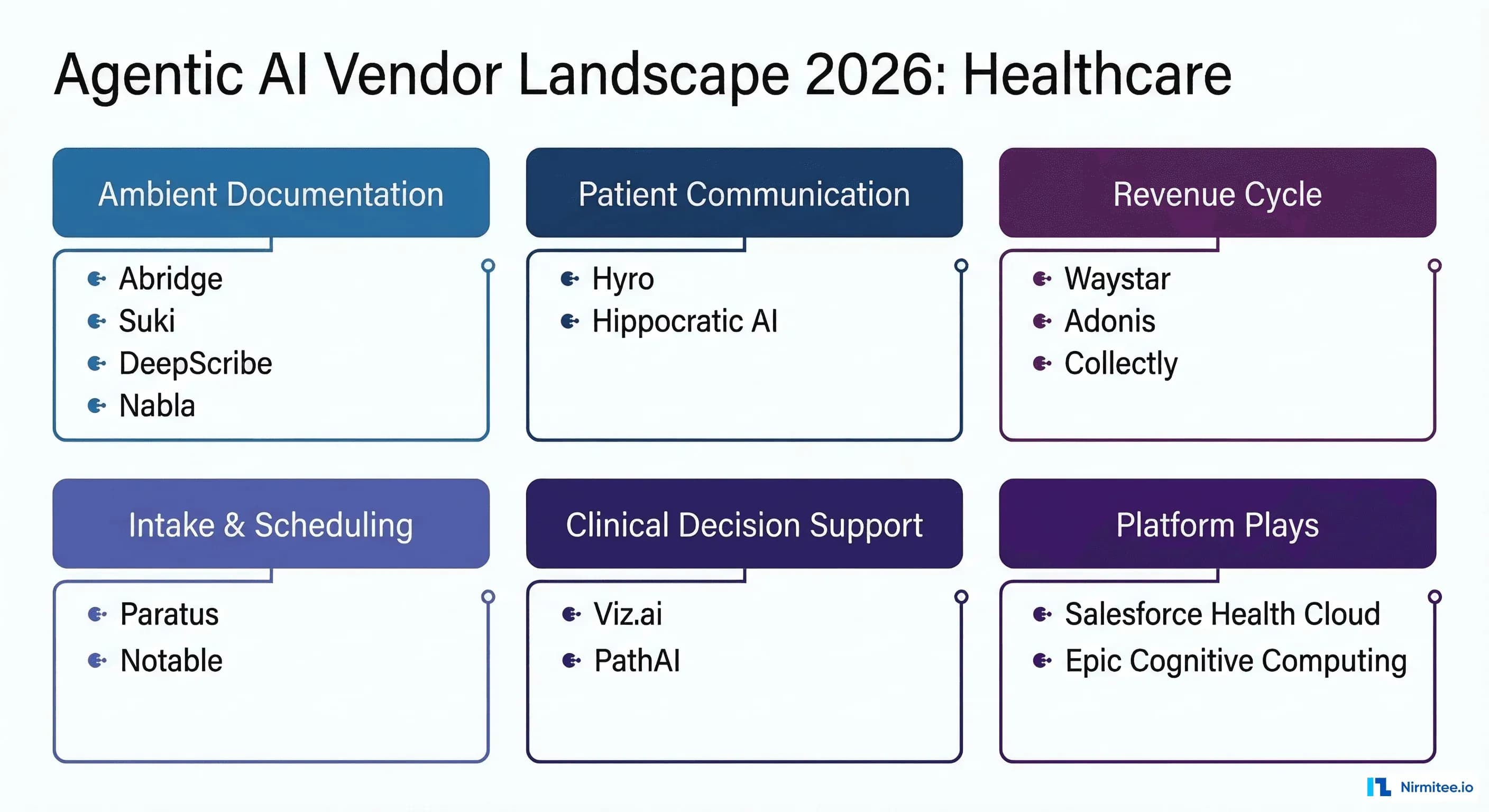

This guide cuts through the noise. We compare 18+ vendors across six categories with engineering-depth analysis of capabilities, integration models, pricing structures, and where each tool actually delivers versus where the marketing gets ahead of the product.

Category 1: Ambient Clinical Documentation

This is the most mature category in healthcare AI, with the clearest clinical evidence. A JAMA Network Open study of 263 clinicians found that burnout decreased from 51.9% to 38.8% after 30 days of ambient AI scribe use—a 13.9 percentage point reduction. The market has stratified into enterprise platforms with deep EHR integration and mid-market solutions with specialty differentiation.

Abridge

What it does: Ambient documentation that generates structured, EHR-ready notes from natural clinician-patient conversations. Named Best in KLAS 2025 and 2026 for ambient AI.

Integration depth: Deep Epic integration via partnership. Notes flow directly into the EHR as structured data, not just text blobs. Uses prior encounter data to maintain consistency across visits.

Funding: $212M total. Backed by a16z, Union Square Ventures, and UPMC.

Best for: Large health systems running Epic that want the safest enterprise bet. Production deployments across multiple major health systems.

Limitation: Epic-centric. If you run Cerner/Oracle Health or athenahealth, the integration is not as deep.

Microsoft DAX Copilot (Nuance)

What it does: Ambient documentation integrated into the Microsoft healthcare ecosystem. Deployed across 600+ healthcare organizations.

Integration depth: Native to Microsoft ecosystem (Teams, Azure, Dynamics 365). Deep Epic integration via Nuance's existing relationships.

Best for: Organizations already invested in the Microsoft stack. The bundling advantage is real—if you are paying for Microsoft 365, Teams, and Azure, DAX Copilot becomes incremental.

Limitation: Vendor lock-in to the Microsoft ecosystem. Customization options are more limited than standalone solutions.

DeepScribe

What it does: Ambient documentation with a focus on specialty care. Achieved a 98.8/100 KLAS score in 2025.

Integration depth: EHR-agnostic with integrations across Epic, Cerner, athenahealth, and others. Specialty-specific AI models for oncology, cardiology, orthopedics, and other complex documentation requirements.

Funding: $53M total.

Best for: Specialty practices and departments where generic documentation AI misses the nuance. Oncology documentation, for example, requires understanding treatment protocols, staging, and response criteria that general-purpose tools handle poorly.

Limitation: Smaller company than Abridge or Microsoft. Less proven at 500+ provider scale deployments.

Suki

What it does: Voice-powered AI assistant that goes beyond documentation to include voice commands for orders, referrals, and patient information retrieval.

Funding: $165M total. Backed by Venrock, March Capital.

Best for: Providers who want hands-free workflow management beyond just note generation. The voice command interface for retrieving patient data and creating orders differentiates Suki from pure documentation tools.

Limitation: Broader scope means less depth in any single capability compared to focused documentation tools.

Nabla

What it does: Ambient documentation with a strong privacy-first architecture. Sub-20 second note generation. Never stores patient data on its servers—audio, transcripts, and notes exist only in the clinician's browser.

Funding: $44M total.

Best for: Organizations with strict data residency requirements or those that want to minimize PHI exposure to third-party infrastructure. European health systems with GDPR requirements.

Limitation: The browser-only architecture limits some integration depth with EHR systems. Smaller deployment footprint than the enterprise players.

Category 2: Patient Communication Agents

This category is where "agentic AI" is most visible to patients. These are not chatbots—they are autonomous agents that handle complete patient interactions end-to-end.

Hippocratic AI

What it does: Patient-facing AI agents for healthcare communication. Has completed over 115 million clinical patient interactions with no reported safety issues. Partnerships with 50+ large health systems, payers, and pharma clients in 6 countries.

Architecture: Constellation architecture with nearly 30 LLMs that support and supervise the main model. Hired 7,000+ U.S.-licensed clinicians for testing. Custom speech recognition with 6% word error rate.

Funding: $404M total at $3.5B valuation. Backed by a16z, General Catalyst, and Kleiner Perkins.

Best for: Health systems and payers that need voice-based patient engagement at scale. The constellation architecture provides safety guardrails that single-model approaches lack.

Limitation: Premium pricing reflects the valuation. Agents do not prescribe or diagnose—they handle communication, coordination, and education tasks.

Hyro

What it does: AI agents for healthcare call centers, scheduling, and patient access. Resolves up to 85% of routine patient interactions autonomously. Deployed across 45+ leading health systems.

Architecture: Hybrid architecture combining LLMs, proprietary Small Language Models (SLMs), and knowledge graphs purpose-built for healthcare. Ranked #1 in time to value—173 days faster than the next solution.

Funding: $95M total. Led by Healthier Capital.

Pricing: Starting at $10,000/month flat rate. Custom enterprise pricing based on call volume and feature set.

Best for: Health systems drowning in call center volume. If your patients wait 8+ minutes on hold for scheduling, Hyro can deflect 85% of those calls to AI within weeks.

Limitation: Focused on patient access workflows. Not a clinical agent—does not handle clinical decision support or documentation.

Category 3: Revenue Cycle Management

Revenue cycle is where AI agents show the most direct financial ROI. The stakes are clear: every percentage point improvement in clean claim rates translates directly to recovered revenue.

Waystar (incorporating Olive AI + Iodine Software)

What it does: End-to-end revenue cycle platform with agentic AI capabilities. Rated #1 in Black Book's Q1 2026 Agentic and Generative AI RCM benchmark. Acquired Olive AI's clearinghouse and patient access assets, plus Iodine Software for clinical documentation intelligence.

Capabilities: AltitudeAI suite covering prior authorization, denial management, coding optimization, and claims processing. Data on 1 in 3 U.S. hospital discharges through Iodine acquisition.

Best for: Health systems wanting a single RCM platform with AI built in. The breadth of data from Iodine gives Waystar a training data advantage that pure-play startups cannot match.

Limitation: Public company (IPO'd) means product evolution is slower than startup competitors. Legacy clearinghouse architecture with AI bolted on, not AI-native.

Adonis

What it does: AI agents specifically for eligibility verification and prior authorization. Task-specific agents that operate autonomously to complete high-volume, rules-driven RCM tasks.

Best for: Organizations that want point-solution excellence in eligibility and PA rather than an end-to-end platform swap.

Limitation: Narrower scope. You will still need other vendors for denial management, coding, and claims.

Collectly

What it does: AI-powered patient billing and collections. Focuses on the patient financial experience, which is increasingly recognized as a critical part of the revenue cycle.

Best for: Health systems with high patient responsibility balances. The patient payment experience directly impacts collection rates and patient satisfaction scores.

Category 4: Intake, Scheduling, and Front-Desk Automation

Paratus Health

What it does: AI operations layer for outpatient clinics. Autonomous agents that fully handle front desk calls, patient intake, insurance verification, documentation, and billing prep. Over 65% of interactions end with positive patient sentiment.

Funding: Y Combinator-backed (W25).

Best for: Small to mid-size outpatient clinics that cannot afford large call center staff. Paratus deploys in as little as 3 weeks—dramatically faster than enterprise solutions.

Limitation: Early-stage startup. Limited to outpatient clinic workflows. Not proven at large multi-hospital scale.

Notable Health

What it does: Automation platform covering patient intake, scheduling, prior authorization, and billing workflows. Combines AI with RPA for end-to-end workflow automation.

Funding: $250M+ total.

Best for: Large health systems that want workflow automation beyond just intake—Notable's platform extends into revenue cycle and care operations.

Limitation: Breadth of platform means some capabilities are shallower than point solutions.

Category 5: Clinical Decision Support and Diagnostics

Viz.ai

What it does: AI-powered care coordination for time-sensitive conditions (stroke, pulmonary embolism, aortic disease). Analyzes medical imaging and routes patients to the right specialist within minutes.

Best for: Hospitals where time-to-treatment directly impacts outcomes. Stroke centers and comprehensive cardiac programs.

PathAI

What it does: AI for pathology diagnostics. Analyzes tissue samples with claims of improved accuracy and consistency over manual pathology review.

Best for: Pathology departments struggling with volume and turnaround time. Cancer diagnosis workflows.

Category 6: Platform Plays

The biggest strategic question in healthcare AI is not which point solution to buy—it is which platform to build on. Two very different strategies are competing for the future. We analyze this in depth in our Salesforce Health Cloud vs Epic AI comparison.

Salesforce Health Cloud + Agentforce

Strategy: CRM-based healthcare platform with AI agents built on Salesforce's Agentforce framework. Partnerships with HealthEx, Verily, and Viz.ai.

Best for: Health systems that want platform-agnostic AI that works across operational systems, not just within the EHR.

Epic Cognitive Computing + Partnerships

Strategy: EHR-native AI through Cognitive Computing platform plus partnerships (Abridge for documentation, Microsoft for infrastructure).

Best for: Epic shops that want the tightest possible EHR integration and are comfortable with the Epic ecosystem.

The Comparison Matrix: What Actually Matters

When evaluating vendors, these are the six dimensions that separate real products from demos:

| Dimension | What to Ask | Red Flags |

|---|---|---|

| EHR Integration Depth | Does data flow bidirectionally? Can the agent write back to the EHR? | Read-only access, screen scraping, or manual copy-paste workflows |

| HIPAA Compliance Model | Where is PHI processed? Stored? Who has the BAA? | No BAA offered, data processed in shared multi-tenant infrastructure without isolation |

| Deployment Model | Cloud only, on-premise option, or hybrid? What about air-gapped environments? | Cloud-only with no path to on-premise for organizations that require it |

| Pricing Transparency | Per-agent, per-transaction, per-provider, or flat rate? | Pricing only available after sales call, no published ranges, hidden usage-based charges |

| Clinical Validation | Peer-reviewed publications? KLAS ratings? Clinical trial data? | No published clinical evidence, only internal benchmarks, testimonials instead of data |

| Auditability | Can you trace every AI decision to the input data and model version? | Black-box outputs with no explanation of reasoning or provenance tracking |

Funding Landscape: Follow the Money

The funding concentration tells a story about market confidence:

| Vendor | Total Funding | Valuation | Latest Round | Signal |

|---|---|---|---|---|

| Hippocratic AI | $404M | $3.5B | Series C (Nov 2025) | Patient communication is a massive market |

| Notable Health | $250M+ | — | Series C | Workflow automation breadth attracts capital |

| Abridge | $212M | — | Series C | Ambient documentation is the leading wedge |

| Suki | $165M | — | Series D | Voice-first interface differentiates |

| Hyro | $95M | — | Growth (Oct 2025) | Call center automation shows fast ROI |

| DeepScribe | $53M | — | Series B | Specialty focus is a defensible niche |

| Nabla | $44M | — | Series B | Privacy-first resonates in EU markets |

| Waystar | Public (IPO) | $4B+ | — | RCM AI is a public-market-scale opportunity |

| Paratus | YC-backed | — | Seed | Clinic operations is underserved |

The Build vs Buy Decision

Not every healthcare AI need should be solved by buying a vendor product. The decision matrix depends on two axes: workflow specificity and integration depth.

Buy when: The use case is well-defined (ambient documentation, call center automation, denial management), multiple vendors have proven solutions, and your differentiation comes from clinical workflows rather than technology.

Build when: Your workflow is highly specific to your organization, you need deep bidirectional EHR integration that vendors do not support, or the use case requires custom agent orchestration across multiple systems. See our framework comparison for building custom healthcare agents.

Hybrid (most common): Buy for commodity capabilities (documentation, scheduling), build the orchestration layer that connects them to your specific workflows, and build custom agents for your differentiated clinical or operational processes.

Vendor Selection Playbook: 90 Days to Decision

- Weeks 1-2: Define use cases and success metrics. Do not start with vendors—start with the clinical and operational problems you are solving.

- Weeks 3-4: Short-list 3 vendors per category based on this guide, KLAS ratings, and peer health system references.

- Weeks 5-8: Proof of concept with top 2 candidates. Insist on using your data, your EHR, your workflows—not the vendor's demo environment.

- Weeks 9-10: Reference calls with health systems of similar size and EHR platforms. Ask specifically about integration challenges, time to value, and ongoing support quality.

- Weeks 11-12: Contract negotiation with clear SLAs, data ownership terms, and exit provisions. Include performance guarantees tied to the metrics from your POC.

The healthcare agentic AI market in 2026 has real products delivering real value. The challenge is no longer "does AI work in healthcare?"—it is selecting the right combination of vendor products and custom-built agents for your specific organization.

At Nirmitee, we help health systems and healthtech companies navigate this landscape. Whether you need help evaluating vendors, building the integration layer between vendor products and your EHR, or developing custom AI agents for workflows that no vendor covers, we bring the engineering depth and healthcare domain expertise to get it right.

Related reading

For more insights, explore our guides on how AI agents are transforming care delivery and FHIR in Modern Healthcare.

You may also find value in EHR Software Development Guide and Building a Healthtech App.